When you're switching health plans, one of the most overlooked but critical factors is generic drug coverage. If you take even one regular medication - like metformin for diabetes, lisinopril for high blood pressure, or levothyroxine for thyroid issues - your out-of-pocket costs can jump by hundreds or even thousands of dollars depending on the plan. Many people assume all plans cover generics the same way. They don't. And that difference can make or break your budget.

How Formularies Work - And Why They Matter

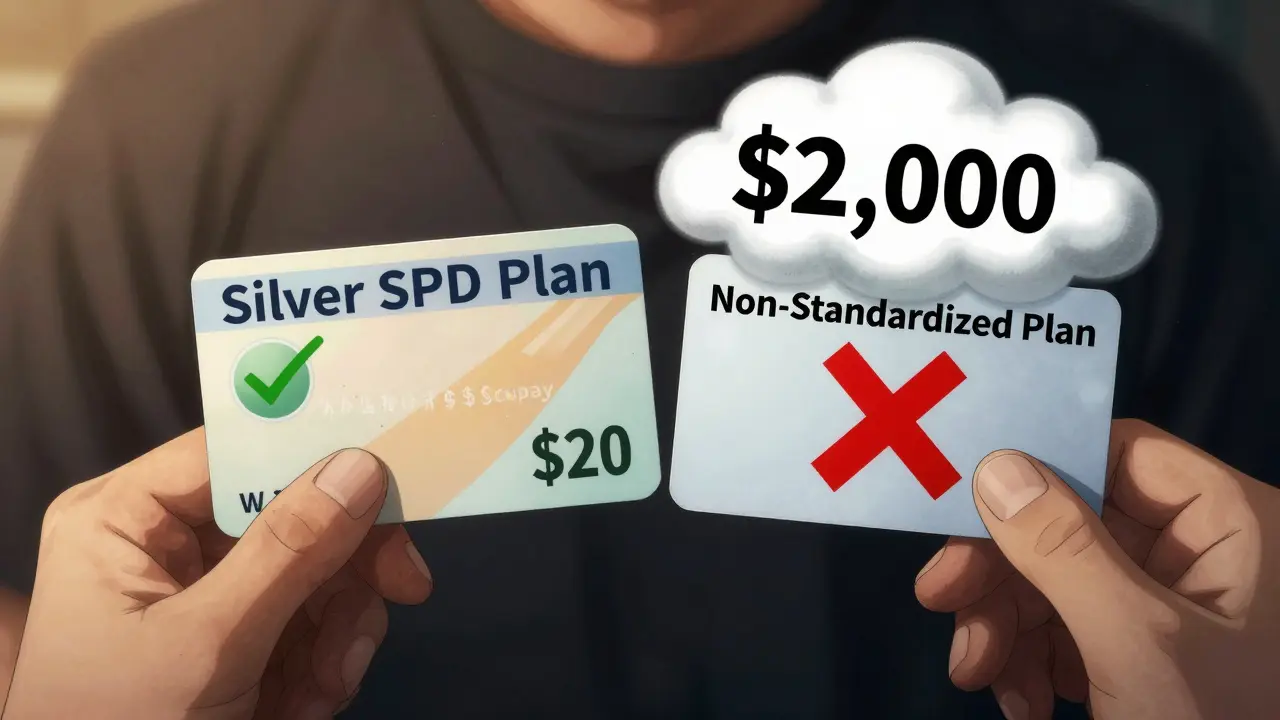

Every health plan has a list of covered drugs called a formulary. This isn't just a random catalog. It's organized into tiers, and each tier has a different cost to you. Tier 1 is almost always reserved for generic drugs. That’s where you’ll find the lowest prices. But here’s the catch: not all Tier 1 drugs are treated equally. In 2023, 92% of private insurance plans used 3- to 5-tier formularies. Medicare Part D plans follow similar structures. The key is knowing which tier your specific medication falls into - and whether the plan waives your deductible for generics. For example, under a Silver Standardized Plan (SPD), which became more common after 2023, you pay a fixed $20 copay for Tier 1 generics - even before you meet your deductible. That means if you need three generic medications a month, you could pay just $60 total, no matter how much you’ve spent on other medical care. In contrast, a non-standardized plan might require you to pay the full deductible - say $2,000 - before any drug coverage kicks in. That’s a $1,500+ difference in a single year.Cost Differences Between Plan Types

Not all plans are created equal. Here’s how costs break down across major plan types:| Plan Type | Generic Copay (Tier 1) | Deductible Waiver for Generics? | Estimated Annual Cost (3 meds/month) |

|---|---|---|---|

| Silver SPD Marketplace Plan | $3-$20 | Yes | $108-$720 |

| Non-Standardized Marketplace Plan | $3-$20 | No | $1,200-$5,000+ |

| Medicare Part D (Base) | $0-$10 | After $505 deductible | $180-$800 |

| Medicare Advantage (MA-PD) | $0-$10 | Often waived | $120-$600 |

| Employer Plan (Basic Option) | $5 | Yes | $180 |

| Employer Plan (Consumer Option) | $10 | No | $360 |

Notice something? The biggest savings come from plans that waive the deductible for generics. That’s why Silver SPD plans are often the best deal for people on regular medications - even if their monthly premiums are slightly higher.

Medicare Advantage plans with drug coverage (MA-PDs) also tend to outperform standalone Part D plans. In 2022, they saved users 18% on average for generic drugs. But here’s the twist: if you only take Tier 1 generics, the difference shrinks because both types use similar copays. The real advantage shows up if you need higher-tier drugs later.

State Rules Can Change Everything

Where you live matters more than you think. California requires a $85 outpatient drug deductible before generics are covered - and then you pay 20% coinsurance up to a $250 cap. New York, on the other hand, waives the deductible entirely for generics and caps copays at $75 for specialty drugs. That means two people with identical prescriptions could pay $0 in New York and $120 in California. States like DC and Oregon have separate drug deductibles, while others bundle them with medical deductibles. These differences aren’t minor. A 2023 KFF study found that states with separate drug deductibles saw 22% higher adherence to medication regimens. Why? Because people actually fill their prescriptions when they know what they’ll pay.

What You Must Check - Step by Step

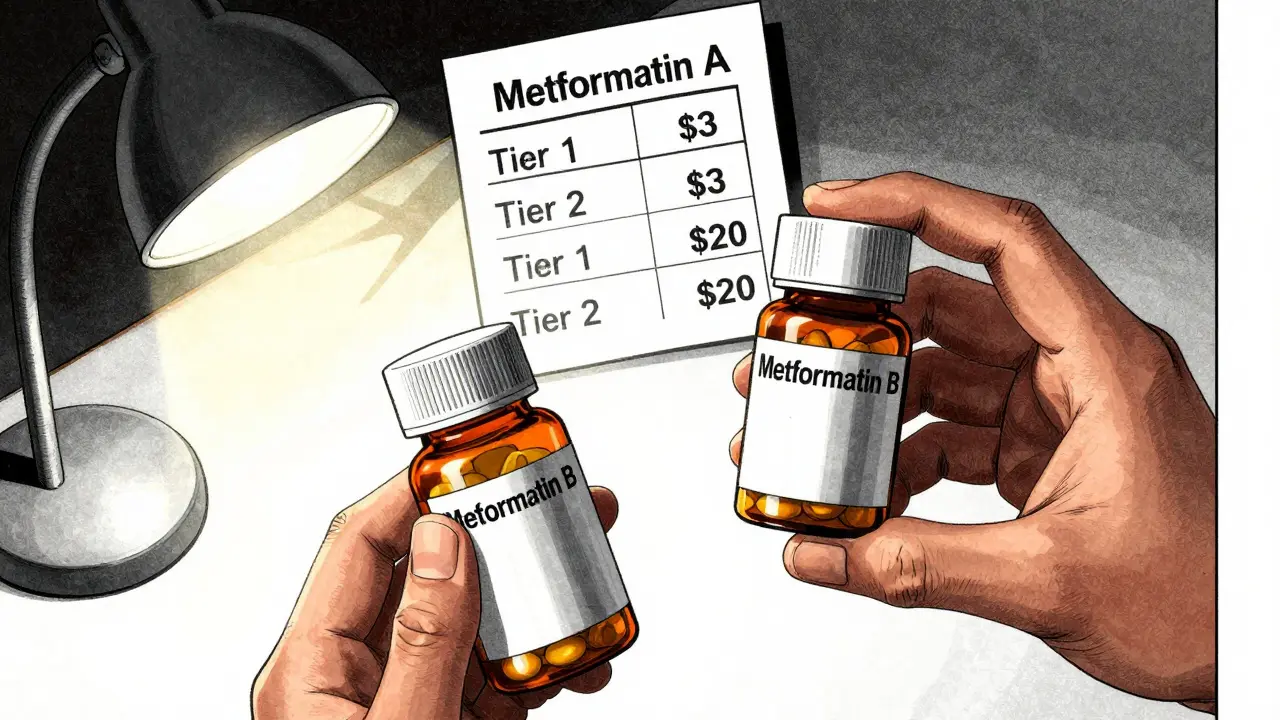

Don’t just look at the plan summary. You need to dig into the details. Here’s a simple four-step process that cuts your risk of surprise costs by 73%:- Get the full formulary - not just the tier list. Look for your exact drug name and manufacturer. For example, “metformin ER 500mg” from Manufacturer A might be Tier 1, but the same drug from Manufacturer B could be Tier 2.

- Verify the formulation - Extended-release, delayed-release, or immediate-release versions can be treated differently. A 2022 American Pharmacists Association study found 68% of people switching plans didn’t check this - and ended up paying 3x more.

- Check the pharmacy network - Your preferred pharmacy might not be in-network. OptumRx data shows out-of-network generic costs can be 300-400% higher. Use the plan’s pharmacy locator tool.

- Run a cost estimate - Use the Medicare Plan Finder (for Medicare) or your insurer’s drug calculator. Input your exact medications, dosage, and pharmacy. These tools are accurate 78-96% of the time.

One user on Reddit switched from a plan with $3 generic copays to one that charged $15 - without realizing her levothyroxine had switched manufacturers. Her monthly cost jumped from $9 to $45. She didn’t catch it until her next refill.

Common Mistakes That Cost Thousands

Most people make these three errors:- Assuming all generics are equal - They’re not. Different manufacturers, even with the same active ingredient, can be in different tiers.

- Ignoring mail-order options - Many plans offer 90-day supplies at lower copays. A $20 monthly copay becomes $50 for three months - a 33% savings.

- Not checking next year’s formulary - Plans change every January. What was Tier 1 in December might be Tier 3 in January. Always re-verify during open enrollment.

UnitedHealthcare alone received over 1,200 complaints in 2023 about unexpected copay increases for generics. One customer wrote: “My $5 generic suddenly became $15. No notice. I had to pay $180 out of pocket for one month.”

What’s Changing in 2025 and Beyond

The rules are shifting fast. Starting in 2025, Medicare Part D will cap total out-of-pocket drug costs at $2,000 per year. That’s huge - but it doesn’t mean lower copays. It means you’ll stop paying after hitting that cap. Also, new tier structures are emerging. Some plans are splitting generics into Tier 1 (preferred) and Tier 1+ (non-preferred), with different copays. This isn’t just complexity - it’s a way for insurers to push you toward cheaper alternatives. And states are stepping in. California’s SB 1423 already requires $0 insulin copays. More states are following. By 2027, experts predict 80% of marketplace plans will drop integrated deductibles for prescriptions entirely - because too many people got burned.Final Tip: Do the Math Before You Switch

Don’t pick a plan based on premium alone. Pick it based on what you spend on meds. If you take three generics a month, calculate your annual cost under each plan. Use this formula:Annual Drug Cost = (Copay per prescription × 12 months × number of meds) + (Deductible × if not waived)

Example: $10 copay × 12 months × 3 meds = $360. If the deductible isn’t waived, add $2,000. That’s $2,360 vs. $360.

That’s not a small difference. That’s life-changing.

Are all generic drugs covered the same across health plans?

No. Even if two generics have the same active ingredient, they can be in different tiers based on the manufacturer, formulation, or whether the plan considers them "preferred." A plan might cover metformin from Manufacturer A at a $3 copay but charge $20 for the same drug from Manufacturer B. Always check the full formulary, not just the tier label.

Should I switch plans just because one has lower premiums?

Not if you take regular medications. A plan with a $50/month lower premium might charge $1,500 more in drug costs over the year. Always calculate total annual cost - premium + deductible + copays. For most people on generics, the lowest premium plan isn’t the cheapest.

How do I know if my medication will be covered next year?

Plans update their formularies every January. You can’t assume coverage stays the same. Review your new plan’s formulary during open enrollment. Use your insurer’s online tool or call customer service. Ask: "Is my exact drug and dosage covered, and what tier is it in?"

What’s the difference between a deductible and a copay for generics?

A deductible is the amount you pay before insurance starts covering costs. A copay is a fixed fee you pay at the pharmacy. Some plans waive the deductible for Tier 1 generics - meaning you pay just the copay from day one. Others require you to meet the full medical deductible first. That’s why Silver SPD plans are better for generics: they skip the deductible entirely.

Can I get my generic drug at a lower cost through mail order?

Yes. Many plans offer 90-day supplies through mail-order pharmacies at a lower copay than retail. For example, a $10 monthly copay might drop to $25 for a 90-day supply - saving you $35 per month. Check if your plan offers this and if your pharmacy is in-network.

15 Comments

Just took my mom to the pharmacy yesterday. She’s on three generics - metformin, lisinopril, and atorvastatin. We checked her new plan’s formulary and found out they switched her metformin to a different manufacturer. Copay jumped from $5 to $18. No warning. She’s 72 and on a fixed income. This isn’t just about money - it’s about survival. Always verify the exact brand, not just the drug name.

Thank you for this breakdown. I’m a pharmacist in rural Ohio, and I see this every single day. Patients assume their meds will cost the same next year. They don’t. I spend 20 minutes a day explaining formulary tiers. Most people just nod and say, ‘I’ll check it later.’ They never do. Please, if you take meds, print out your formulary. Keep it in your wallet. It’s that important.

I spent six months comparing plans after my husband’s employer changed carriers. We take five generics - two for his diabetes, one for blood pressure, one for cholesterol, and one for thyroid. The difference between a Silver SPD and a ‘low-premium’ plan was $2,100 a year. We picked the more expensive plan. We saved $1,800. The math doesn’t lie. I made a spreadsheet. I color-coded everything. I even called customer service three times asking, ‘Is this the same exact formulation?’ They got tired of me. Worth it.

Oh wow, another bleeding-heart liberal post about how ‘insurance is unfair.’ Let me guess - you’re also mad that your $20 generic now costs $22 because the manufacturer changed? Newsflash: the market adjusts. If you want cheaper drugs, stop complaining and move to Canada. Or better yet - stop taking them. Maybe your body will heal itself. I’m sure your thyroid will thank you for the ‘natural detox.’

Yall be overthinkin this. Just go to Walmart. $4 generics. Done. No formulary. No tier. No deductible. Just walk in, pay $4, walk out. Why you even need a plan? You ain’t got no choice? Then you ain’t got no problem. Simple. I got my metformin for $3.50. No cap. No fine print. Just cash. You overthinkers need to chill.

I’m Irish and I moved to the US last year. I had no idea this was such a mess. Back home, I get all my meds for €2 a month. Here? I got a $1,200 deductible and my levothyroxine is on Tier 2? I cried in the pharmacy. I didn’t know I was signing up for a financial obstacle course. I’m still trying to figure out mail-order. Is it safe? Can I trust it? I need help.

My sister in Delhi takes the same generic as I do here in Mumbai - same dosage, same manufacturer. She pays $0.50. I pay $12. The difference? Insurance. Not quality. Not efficacy. Just bureaucracy. If you’re on generics, you’re already in the 90th percentile of global health access. Don’t let the system make you feel guilty for wanting to afford your meds. You deserve it.

My cousin switched plans last year because the premium was $30 cheaper. Ended up paying $900 extra on meds. He didn’t know his insulin was now a Tier 2. He ran out. Had to go to the ER. Now he’s on Medicaid. Lesson: cheap premium ≠ cheap total. Always run the numbers. And if you’re on meds, talk to your pharmacist. They know more than your insurance rep.

They did this on purpose. You think it’s an accident that plans make generics harder to access? No. They want you to skip doses. They want you to go to the ER. Then they bill you for $5,000. It’s not incompetence - it’s strategy. I work in billing. I’ve seen the reports. They track non-adherence. They profit from it. So yes - check your formulary. But also - fight back. Call your rep. File a complaint. Write to your senator. This isn’t healthcare. It’s a racket.

There’s a philosophical dimension here we rarely acknowledge: the commodification of health. When your ability to access a life-sustaining drug hinges on a tiered formulary determined by profit margins, we have to ask - what does it mean to be human in a market-driven system? The fact that a $3 metformin can become a $20 burden isn’t a flaw in the system - it’s the system working as designed. The real question isn’t how to navigate formularies - it’s whether we should tolerate a system that turns survival into a financial calculation.

Y’all are making this sound like rocket science. It’s not. Think of it like grocery shopping. You don’t buy the most expensive cereal because it’s got a fancy label. You check the price per ounce. Same with meds. Look at the total cost - not the monthly premium. If your plan makes you pay $2,000 before your $5 copay kicks in - that’s like buying a $2,000 box of cereal just to get the $5 bag. Don’t be that person. Do the math. Use the calculator. It’s right there. Click it. You got this.

Here’s the real problem: 80% of people don’t even know their own meds are on Tier 2. They think ‘generic’ means ‘cheap.’ It doesn’t. I’ve seen patients cry because their ‘$3’ drug became ‘$45.’ Why? Because the manufacturer changed. And the plan didn’t notify them. No email. No letter. Just a surprise bill. That’s not negligence - it’s fraud. Someone should get sued for this.

PLEASE PLEASE PLEASE check your pharmacy network!!! I went to CVS and paid $80 for my generic because my plan only covered Walgreens. I didn’t know! I cried. I called my insurance - they said, ‘It’s on your plan documents.’ I didn’t read 147 pages! Now I use the pharmacy locator tool. I screenshot it. I keep it on my phone. I even texted my mom the link. She’s 68 and she gets it now. You can too. Don’t be like me. Check. It. Now. 💔🙏

Ohhh so now we’re all supposed to be pharmacists? Let me guess - next you’ll tell us to memorize the ICD-10 codes for our own pills. I took metformin for 10 years. Never checked the formulary. Still alive. My body didn’t implode. Maybe your meds aren’t as essential as you think. Just take them when you can. Or don’t. Maybe the universe has a plan. Or maybe you’re just too lazy to do your homework. Either way - chill.

It is important to note that while the data presented is largely accurate, the assumption that all patients have equal access to online tools or digital literacy is flawed. Many elderly, low-income, and non-native English speakers rely on in-person assistance. The onus should not be on the patient to navigate complex formularies. Healthcare systems must provide clear, accessible, and proactive guidance. The current model places an unreasonable burden on vulnerable populations. Reform is not optional - it is necessary.