Ever paid $10 for your generic blood pressure pill and thought, "Great, I’m one step closer to hitting my deductible"-only to find out at year-end that your deductible is still untouched? You’re not alone. Millions of people assume that every copay they make counts toward their deductible. But here’s the truth: generic copays don’t count toward your deductible. They do count toward your out-of-pocket maximum. And that difference? It can save you thousands-or cost you thousands-if you don’t understand it.

What’s the difference between a deductible and an out-of-pocket maximum?

Your deductible is the amount you pay out of pocket before your insurance starts sharing costs. For example, if your deductible is $2,000, you pay the full cost of covered services (like doctor visits or lab tests) until you’ve spent $2,000. After that, you usually pay coinsurance-say, 20%-while your insurer covers the rest.

Your out-of-pocket maximum is the total you’ll pay in a year for covered services. Once you hit that limit, your insurance pays 100% of everything else for the rest of the year. For 2026, the federal cap is $10,600 for individuals and $21,200 for families on Marketplace plans. This number includes your deductible, coinsurance, and yes-copays.

Here’s the key: deductible is the first hurdle. Out-of-pocket maximum is the ceiling. Copays help you climb toward the ceiling, but they don’t knock down the first hurdle.

Why don’t generic copays count toward your deductible?

This isn’t a glitch-it’s by design. Before the Affordable Care Act (ACA) in 2014, many plans didn’t even count copays toward anything. People paid $15 for insulin, $20 for asthma inhalers, and saw zero progress toward their deductible or any financial protection. That changed with the ACA. The law required all cost-sharing-including copays-to count toward the out-of-pocket maximum. That was a win for chronic illness patients who need daily meds.

But the ACA didn’t eliminate deductibles. It just added a new layer: the out-of-pocket maximum. So now, most plans have two tracks:

- Track 1: Deductible - You pay full price for services until you hit this number. Copays usually don’t count here.

- Track 2: Out-of-pocket maximum - Every dollar you spend on in-network care (deductible, coinsurance, copays) counts here. Once you hit it, insurance pays 100%.

For example: You have a $1,500 deductible and $10 generic drug copays. You fill 200 prescriptions in a year. That’s $2,000 in copays. You’ve paid $2,000 total-but your deductible is still $1,500 short. Your out-of-pocket maximum? You’re already halfway there (assuming your max is $6,000). You’re not closer to meeting your deductible. But you’re getting closer to free care for the rest of the year.

How do different plan designs affect this?

Not all plans are the same. There are three main structures:

- Single deductible - One number covers both medical and prescriptions. If you pay $10 for a generic, it counts toward this one deductible. This is rare-only 27% of employer plans use it.

- Separate medical and prescription deductibles - You have two deductibles. You might pay $1,500 for doctor visits and $1,000 for prescriptions. Copays don’t count toward either until you meet those separate thresholds. This is the most common setup-used by 37% of plans.

- Copay-only (no prescription deductible) - You pay your $10 copay right away, no deductible to meet. But again, that $10 doesn’t help your medical deductible. It only counts toward your out-of-pocket maximum. This is used by 36% of plans.

If you take daily meds, you want to know which type you have. A 2023 survey found 68% of consumers mistakenly believe their copays count toward their deductible. That misunderstanding leads people to skip meds, thinking they’re "already covered"-when they’re actually still paying full price.

Real-world impact: Stories from the front lines

"I paid $10 for my diabetes meds every month for a year. I thought I was working toward my $2,000 deductible," says Maria, 54, from Ohio. "When I got my Explanation of Benefits, I saw I’d paid $1,200 in copays-but my deductible was still $1,980. I was furious. I didn’t even know copays didn’t count. I could’ve saved money if I’d just switched to a plan with a lower deductible or a single deductible structure."

On the flip side, people with high-cost conditions are benefiting. "I hit my $8,500 out-of-pocket max last October," says James, 61, from Michigan. "I’ve been on insulin since 2018. Before 2014, my copays didn’t count for anything. I’d pay $45 a month and feel like I was throwing money away. Now? After October, my insulin was free. That’s life-changing."

These aren’t edge cases. The Congressional Budget Office estimates that confusion around cost-sharing leads to $15 billion in avoided prescriptions each year. People skip meds because they think they’ve "met" their deductible. They haven’t. And the consequences? Hospitalizations, complications, higher long-term costs.

What should you do to avoid the trap?

Don’t guess. Don’t assume. Check your plan documents. Here’s how:

- Find your Summary of Benefits and Coverage (SBC). It’s required by law and must be provided before enrollment. Look for a table titled "Cost-Sharing" or "How You Pay."

- Check the "Does this count toward my deductible?" column next to "Generic Prescription Drugs." If it says "No," you’re in the majority.

- Look for the out-of-pocket maximum. That’s your real safety net. If you take daily meds, track how much you’re paying in copays. Add it to any coinsurance or deductible payments. You’ll know when you’re close to hitting your cap.

- During open enrollment, compare plans. Some now offer a "combined deductible"-where prescriptions count toward the same deductible as doctor visits. These are becoming more common. In 2025, 68% of Blue Cross plans use this model. By 2027, McKinsey predicts 60% of insurers will offer at least one plan like this.

What’s changing in 2025 and beyond?

The government is pushing for clearer communication. Starting in 2025, all insurance documents must clearly state: "Your copays count toward your out-of-pocket maximum but not your deductible." No more fine print.

Five states are testing "integrated deductible" models, where prescription copays count toward the main deductible. Early results show 28% more people stick to their meds. That’s huge for chronic conditions like asthma, diabetes, and high blood pressure.

But there’s a trade-off. If you combine everything, premiums might rise 3-5%. Insurers argue that simpler rules mean higher costs. Consumers argue that simpler rules mean fewer people skip meds. The debate isn’t over.

Bottom line: Know your plan, track your spending

Generic copays don’t help you meet your deductible. But they do help you hit your out-of-pocket maximum. That’s the real win. Once you hit that cap, your meds, your doctor visits, your hospital stays-all of it-is covered. No more surprises. No more bills.

Don’t let confusion cost you your health. Open your plan documents. Find the SBC. Look for the words "copay" and "deductible." If they’re separate, you’re not alone. But now you know how it works. Track your spending. Know when you’re nearing your limit. And if you take daily meds, you might just be one year away from paying $0.

Do generic drug copays count toward my deductible?

No, generic drug copays typically do not count toward your medical deductible. They are considered a separate form of cost-sharing. Your deductible is usually only met by paying full prices for services (like doctor visits or lab tests) before your insurance starts sharing costs. However, these copays do count toward your out-of-pocket maximum, which is the total amount you’ll pay in a year before your insurance covers 100% of covered services.

What counts toward my out-of-pocket maximum?

Your out-of-pocket maximum includes all in-network cost-sharing: your deductible, coinsurance, and copays for doctor visits, prescriptions, lab tests, and hospital stays. It does not include your monthly premiums or services you receive out-of-network (unless your plan allows it). Once you’ve paid the full amount of your out-of-pocket maximum in a year, your insurance covers 100% of all covered services for the rest of that year.

Can I meet my deductible just by paying copays?

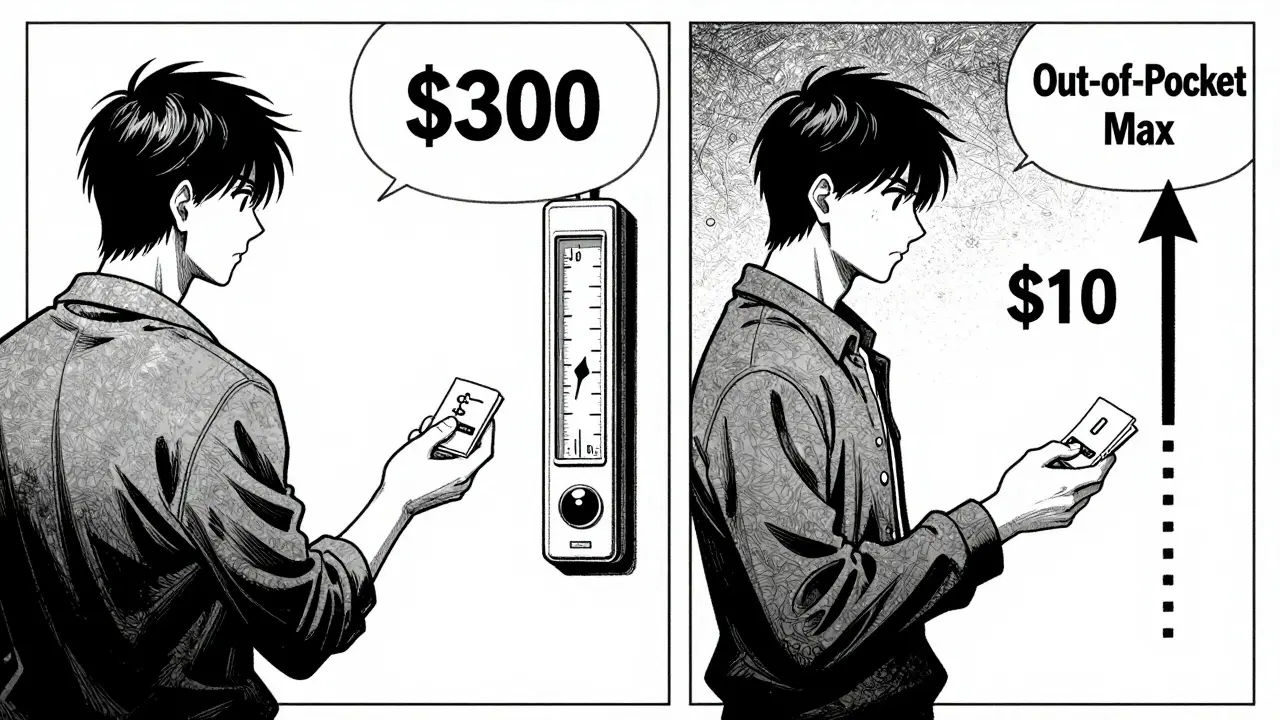

No. Paying copays alone will not help you meet your deductible. Most plans treat copays as a fixed fee you pay at the time of service, separate from the deductible. The deductible is only met when you pay the full cost of services (not just a copay) until you reach that dollar amount. For example, if your deductible is $2,000, you must pay $2,000 in full charges before coinsurance kicks in-even if you’ve paid $3,000 in copays.

Why do some plans have separate prescription deductibles?

Separate prescription deductibles allow insurers to manage drug costs differently from medical costs. They’re often used in plans with high-cost medications. You pay full price for prescriptions until you meet the prescription deductible, then pay a copay or coinsurance. This structure keeps premiums lower but increases short-term costs for people who need regular meds. About 37% of employer plans use this model. Always check your plan’s Summary of Benefits and Coverage to see if you have one.

What should I look for in my insurance documents?

Look for the Summary of Benefits and Coverage (SBC)-it’s required by law and must be provided before you enroll. Find the section on "Cost-Sharing" or "How You Pay." Check the row for "Generic Prescription Drugs" and see if it says "Yes" or "No" under "Counts Toward Deductible?" Also, find your out-of-pocket maximum. Track your copays throughout the year. If you take daily meds, knowing how much you’ve paid helps you predict when your insurance will start covering 100%.

Understanding how your insurance works isn’t just about saving money-it’s about staying healthy. If you’re on daily medication, knowing where your copays go can mean the difference between sticking to your treatment plan and skipping doses because you think you’ve "met" your deductible. You haven’t. But you’re getting closer to the real finish line: your out-of-pocket maximum. And when you hit it? That’s when your care truly becomes affordable.

11 Comments

Okay but like… I just found out my $15 insulin copay doesn’t count toward my $3,000 deductible? I’ve been paying that for 18 months and thought I was "almost there." Turns out I’m at $270 toward my OOP max and $0 toward my deductible. My bank account is crying. 😭

WAIT. WAIT. WAIT. You mean to tell me I’ve been paying $20 a month for my asthma inhaler for THREE YEARS… and NONE of it went toward my deductible?!?!?!?!?!?!?!?!? I thought I was building equity in my health plan like a mortgage!! I feel so used!! I need a nap and a therapist!!

This is actually one of the most important things I’ve read all year. Seriously. I’ve seen so many people panic because they think they’re "done" with costs after a few copays. But the out-of-pocket max? That’s the real finish line. Once you hit it, everything’s free. So keep filling those prescriptions. You’re not wasting money-you’re investing in your future free care. 🙌

Let me paint you a picture: imagine your deductible is a locked door. Copays? They’re like shiny coins you keep dropping into a slot beside it. You can hear them clink, feel like you’re doing something, but the door stays shut. The out-of-pocket max? That’s the keycard you’re collecting one swipe at a time. Eventually, you’ll glide right through. It’s not fair-but it’s the game we’re playing. Learn the rules, play smart.

OMG I just checked my SBC and it says "NO" next to generic drugs counting toward deductible 😭 I’m so mad I can’t even. I thought I was being responsible. Turns out I’m just a pawn in Big Insurance’s chess game. And my pharmacist? She just smiles like she knows something I don’t. 🤬

The premise is misleading. Copays were never intended to count toward deductibles. That’s why they’re called "copays"-not "contributions." The ACA didn’t "fix" anything; it just shifted financial burden from insurers to consumers under the guise of protection. The real issue? People don’t read their own contracts. Blame the consumer, not the system.

I’m so glad someone finally explained this clearly. I’ve been helping my mom navigate her Medicare Advantage plan, and she was convinced her $10 copays were "counting." We sat down, found the SBC, and she cried-because she realized she’d been skipping doses thinking she was "covered." Now she’s on track to hit her OOP max in July. This info saves lives.

Yessss!! 🌈💖 I’ve been telling my friends this for years! Copays = stepping stones to your OOP max, NOT the deductible. Keep taking your meds! You’re not wasting money-you’re building your freedom. One day, you’ll look back and be like, "Wait… I didn’t pay for that?" 😎🩺

Another socialist scam. Insurance was never meant to be free. If you can’t afford your meds, don’t take them. Or move to a country where the government pays for your mistakes. America built itself on personal responsibility-not handouts disguised as "affordable care." You want free meds? Work harder.

This is all fake. The government and pharma companies are hiding the truth. Your copays DO count toward deductible. They just hide it in the fine print. They want you to think you're safe so you keep buying pills. Soon you'll be on 12 drugs a day and they'll own you. Check the source. It's all connected to the vaccine chip.

After reading this, I went back to my 2024 EOBs and totaled up my copays-$1,800. I thought I was halfway to my deductible. I was actually 30% of the way to my OOP max. I’m not mad. I’m motivated. This changes everything. Thank you for this. I’m sharing it with everyone I know.